[ CYPHER CODE #1241 ]

Migration into Vegas is slowing sharply.

[ CYPHER CODE #1242 ]

Rising apartment vacancies often signal trouble before home prices fall.

[ CYPHER CODE #1243 ]

When demand fades, the housing boom fades with it.

BRIEFING

Grant here. Not long ago, Las Vegas was one of the top-growing cities in America. Post pandemic, people were flocking to Vegas like crazy, mainly to escape growing housing prices and high taxes in nearby states. But that boom is ironically creating a massive vacuum, and now, Vegas' apartments are filled more with tumble weeds rather than tenants. Let’s break it down.

You'd think that the early warning signs of economic downswings would be the housing market or home prices. But no, it’s the rental market. Because when apartments start sitting empty and landlords begin cutting rents to attract tenants, it can signal that supply-and-demand are flipping upside down.

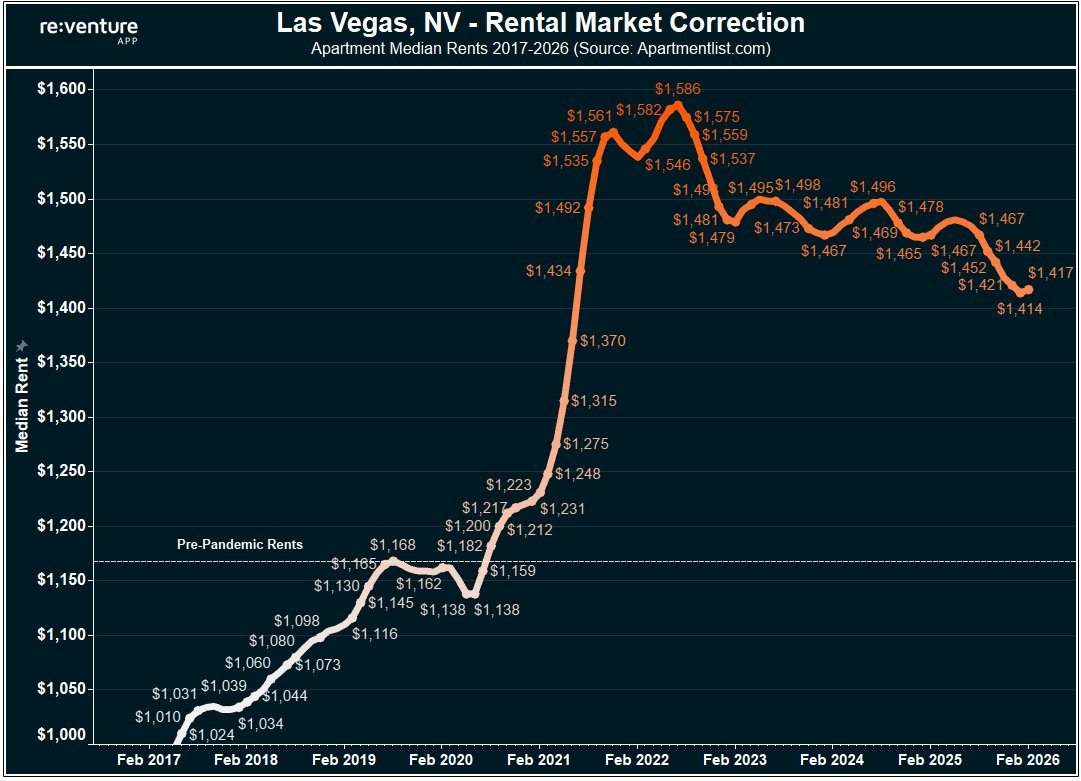

A new thread examining Las Vegas housing data highlights a noticeable rise in apartment vacancies across the metro area. Roughly 7.6% of Vegas apartments are now sitting empty, the highest vacancy rate the city has seen in nearly a decade. To put that in perspective, vacancies during the height of the pandemic housing boom dropped as low as 2.4%.

That means today’s vacancy rate is more than triple the pandemic low.

Landlords who were raising rents aggressively just a few years ago are now moving in the complete opposite direction, which is never a good sign. In many cases, rents are being cut and incentives are being offered just to get tenants through the door. Some are even throwing in a full month free of rent.

According to Apartment List, the average rent in Las Vegas peaked around $1,586 in 2022 during the post-pandemic housing surge. Today that number has fallen to roughly $1,417.

While rents are still about 21% higher than they were before the pandemic, things definitely don't look to be heading in the right direction.

SOURCE

Las Vegas apartment vacancies are spiking.

And landlords are not happy.

7.6% of Vegas apartments are now sitting vacant, the highest level in nearly 10 years.

(Triple the pandemic low of 2.4%).

4 years ago, rents were soaring, and there was no availability.

Now they're… pic.twitter.com/4tNAZPo2Y6

— Nick Gerli (@nickgerli1) March 6, 2026

SOURCE

Las Vegas apartment vacancies are spiking.

And landlords are not happy.

7.6% of Vegas apartments are now sitting vacant, the highest level in nearly 10 years.

(Triple the pandemic low of 2.4%).

4 years ago, rents were soaring, and there was no availability.

Now they're cutting rents aggressively and giving concessions just to get tenants through the door.

A potentially ominous sign for Vegas' overall housing market in 2026.

1) I like looking at a local area's rental market as an additional bellwether of where things are heading.

If vacancies are rising, and rents are getting cut, it's a suggestion that the broader housing market is oversupplied.

And that general housing deflation could be on the way (as if the case in Las Vegas).2) Data from Apartment List shows that apartment rents in Vegas are down about 10% from their post-pandemic peak in 2022.

Back then, they were at $1,586 per apartment.

Now they're at $1,417.

3) In some communities, the cuts could be even steeper.

Here is an apartment community that has 1-month free.

On 600 SF studios at $725/month base rent.

($664 net of concession)

4) The reason why this is happening is multi-fold.

First, Las Vegas is experiencing a slowdown in net migration after the pandemic, both from domestic and international sources. This is crimping housing demand.

Second, the affordability metrics in Vegas became skewed after the pandemic, and many local renters, especially those on the lower end of the income spectrum, became priced out.

Third, the local economy in Las Vegas is starting to struggle. Job growth in the metro just went into negative YoY territory for only the 4th time in the last 35 years.

5) Nevada non-farm payrolls hit -0.6% YoY in December 2025, which is the first negative reading since the pandemic.

And only the 4th since 1992.

Indicating how robust Vegas' job growth usually is.

6) But no longer. Slower job growth, due to reduced tourist demand and potentially lower immigration, is weighing the rental market.

At the same time, there's been a marked slowdown in migration from other U.S. states, which is causing a reduction in home sales and buyer demand.

In fact - demand to buy houses in Vegas in Jan 2026 was 43% below the pandemic peak.

7) Home values are now also officially dropping in Vegas' housing market. They're down -2.2% YoY.

But still up 35.8% over the last five years.

8) The value drops are getting especially intense in certain ZIP codes.

Some areas are down over 6% in the last year, according to Zillow's value index, which is a big drop for just one year.

DEBRIEFING

Unlike a lot of cities that rely on more stable industries like government or technology, Vegas runs heavily on tourism, hospitality, and entertainment, which are fairly volatile industries. That means when the economy is booming, Vegas explodes with growth. But when things begin to cool, Vegas is often one of the first places where cracks start to appear.

None of this necessarily means that a housing crash is 100% around the corner. But historically, when the rental market starts showing signs of weakness in a place like Las Vegas, it often signals a bigger shift is starting to happen.

NOW YOU KNOW

What happens in Vegas doesn’t always stay in Vegas. Sometimes it’s a preview of what’s coming next.

Share your opinion

COMMENT POLICY: We have no tolerance for comments containing violence, racism, vulgarity, hard-core profanity, all caps, or discourteous behavior. Thank you for partnering with us to maintain a courteous and useful public environment!

Article has some good data, but one that is curiously missing is inventory. In the research for this, did you check the available inventory for multifamily dwellings? If you had, you may have found that land developers have been building new communities nonstop for the last 6-8 years, vastly outpacing previous residential development. The migration and jobs data provided is not a great forecast for Las Vegas to be sure and gaming is in trouble too.